Watch out below for a falling loonie

Article content

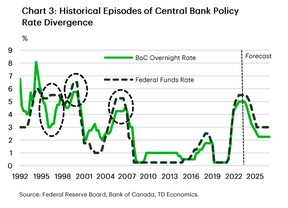

The Bank of Canada and Federal Reserve are likely to part ways soon — whether it is this week or next month — and that could mean trouble for the Canadian dollar.

While Canada’s central bank is close to cutting its interest rate, the Fed is not, and the ensuing gap between policy rates could have “knock-on effects,” economists warn.

To determine the impact of those effects TD Economics looked back at other times in recent history when the Bank of Canada has had to go it alone.

Advertisement 2

Article content

“The pertinent question is not ‘if’ the BoC can cut ahead of the Fed, but by how much,” wrote Toronto Dominion economists James Orlando and Brett Saldarelli.

Historically, a difference of 100 basis points looks to be the comfort zone, but as the following examples show the gap has sometimes yawned considerably wider.

Take the Mexican peso crisis in 1994-95, when the Bank of Canada had to slash its rate from 8.1 per cent to 3 per cent as the economy took a hit. In circumstances eerily similar to today, Canada’s GDP was so weak that supply was outstripping demand and inflation was slowing.

The U.S. economy was in much better shape, allowing the Fed to make only modest adjustments to its rate. By early 1997 the difference between the two countries’ interest rates was a “whopping 250 basis points,” said the economists.

Rising energy prices were a buffer to the Canadian dollar then, but when the Asian and Russian financial crises slammed commodity prices, the loonie fell to 63 US cents.

“To defend the loonie, the BoC hiked one last time in the summer of 1998 (by an additional 100 bps), closing the policy rate gap with the Fed,” said the economists.

Posthaste

Article content

Advertisement 3

Article content

The loonie fell to a record low of 62 US cents the next time the two central banks diverged. It was 1999 and the Fed briefly intervened to quell market chaos in the aftermath of the collapse of billion-dollar hedge fund Long-Term Capital Management.

But as the economy continued to expand, concerns about inflation grew and the Fed began raising rates halfway through the year. The Bank of Canada followed the Fed’s lead but at a slower pace, causing the rate gap to reach 75 bps by mid-2000.

By the end of that year, the Canadian dollar had slid to 64 US cents, helped by weak commodity prices and market volatility, and then bottomed out at 62 US cents in 2002, said the report.

The third episode preceded the great financial crisis. Between 2003 and 2006 the Fed was forced to hike its rate by more than one per cent above Canada’s as rapidly rising real estate prices spurred the economy. This time though soaring commodity prices — the price of oil doubled over the four years — pushed the loonie up to 91 US cents and past parity in 2007.

What happened next is history. The bottom fell out of the U.S. economy in the worst recession since the Great Depression, and the Fed slashed rates to the zero lower bound, where they remained for the next seven years.

Advertisement 4

Article content

So what does all that mean for 2024?

Unfortunately, oil prices likely won’t come to the loonie’s rescue this time.

As Charles St-Arnaud, chief economist at Alberta Central, pointed out in an earlier report, the days of Canada’s petrocurrency are over.

A decline in investment in Canada’s oil industry and more money flowing to investors, many of them foreigners, has meant that oil prices are not giving the Canadian dollar the boost they once did.

With Canada’s economy lagging the U.S., TD predicts the Bank of Canada will begin cutting rates this summer and increase the pace at the end of 2024. Down south, the Fed likely won’t start cutting until December, and eventually the gap between the two rates will widen to 125 basis points.

“This could risk the currency dropping below the psychological 70 US cent level should a risk-off event, such as an intensification of geopolitical tensions, occur,” said Orlando and Saldarelli.

Sign up here to get Posthaste delivered straight to your inbox.

The last data point before the Bank of Canada’s interest rate decision on Wednesday is in and it now looks increasingly likely that a cut is in the cards.

Advertisement 5

Article content

Market bets on a cut this week rose to 80 per cent after the gross domestic product data came out Friday.

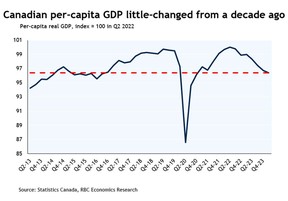

GDP rose 1.7 per cent in the first quarter of 2024 and was revised down in the fourth quarter of 2023, adding up to a smaller gain than expected.

When measured against population growth, per capita GDP fell for the sixth quarter out of seven, leaving output little changed from a decade ago, said Nathan Janzen, assistant chief economist at the Royal Bank of Canada.

“The downside surprise in Canada’s Q1 GDP growth likely removes the last potential barrier preventing the BoC from easing off the monetary policy brakes with an interest rate cut next week,” said Janzen after the data came out.

Some though are not yet convinced. Capital Economics is sticking to its call for a July cut, arguing that the numbers may not yet be enough to sway the central bank.

“With consumption growth strong, … we still think the odds slightly favour delaying until July,” said Capital.

Only time will tell.

- Calgary will release home sale numbers for May today, followed by Vancouver on Tuesday. Toronto homes sales are expected on Wednesday.

- Today’s Data: United States construction spending, ISM manufacturing

Advertisement 6

Article content

Recommended from Editorial

The old retirement rule of thumb was to amass $1 million in savings for your golden years. But certified financial planner Allan Norman says that kind of safety net comes with a risk called regret — regret that you didn’t do things when you could have or when they had more meaning for you. Find out more.

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line with your contact info and the gist of your problem and we’ll try to find some experts to help you out, while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers, led by Julie Cazzin, can give it a shot.

Advertisement 7

Article content

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Plus check his mortgage rate page for Canada’s lowest national mortgage rates, updated daily.

Today’s Posthaste was written by Pamela Heaven, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content