After two tough years, activity is expected to pick up — but even rebounds have risks

Article content

Peter Miller doesn’t mince words when describing the dealmaking doldrums that Bay Street has slipped into over the past couple of years. But the head of global equity capital markets at BMO Capital Markets and other investment bankers are cautiously optimistic that the action is about to pick up, and anxious to talk about the reasons why.

“You know, 2023 was a tough year,” Miller said in a recent interview, pointing out that new issue activity barely matched levels reached in a “weak” 2022.

Advertisement 2

Article content

The primary culprit, he and other investment bankers said, was uncertainty, as questions about how high interest rates would go — and how quickly they might come down once they peaked — kept a lid on activity.

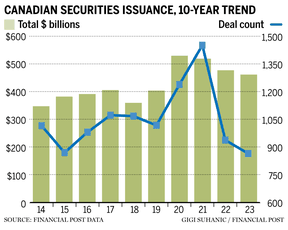

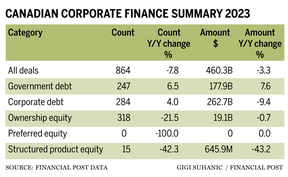

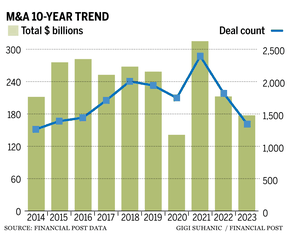

There were fewer deals overall last year — 864 compared to 937 in 2022 — according to figures from Financial Post Data. The total value of all deals also declined, to $460.3 billion from $475.7 billion a year earlier.

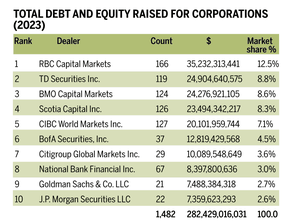

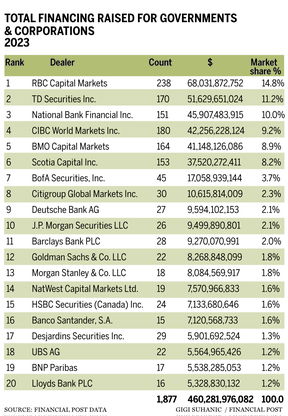

RBC Capital Markets topped 2023’s all-deals category, which includes corporate debt and equity as well as government debt issues, with a 14.78 per cent share. RBC had 238 mandates and $68.03 billion in deals, according to Financial Post Data. TD Securities, the investment banking division of Toronto-Dominion Bank, came second in the all-deals ranking with an 11.22 per cent share on 170 mandates and a dollar figure of $51.63 billion. National Bank Financial rounded out the top three for all deals with a 9.97 per cent market share 151 mandates and $45.91 billion in deals.

It was a far cry from the dealmaking frenzy of 2020 and 2021, when interest rates remained at historic lows, making capital accessible and cheap, and pent-up demand helped drive a post-shutdown boom in activity. More than a thousand deals were done in each of those years, with combined values topping $500 billion each year.

Advertisement 3

Article content

Now, with a widespread consensus that rates have likely peaked and will start coming down later this year, a view that propelled markets higher as 2024 approached, there is hope on Bay Street that the year ahead will see some of that momentum return.

“Issuers are now convinced that peak rates are behind us, and you’ve seen this massive rally in the equity market since late October,” Miller said. “Now, instead of saying, ‘Well, how high is it going to go?’ They’re saying, ‘How low is it going to go and how quick?’”

He cautioned that a return to better times may take a little time if the market has overreacted. Hopes of an early-year interest rate cut were dampened with the release of minutes from the Federal Reserve’s most recent rate setting session, for example.

“But the important point is that inflection has taken place,” Miller said. “We need to see the peak rates behind us and then we’re going to see action.”

An uptick in activity will be welcome across the board, but particularly in the equity markets, which last year saw just 333 deals, down from 432 in 2022 and fewer than half the 861 done in 2021. The overall tally of $19.8 billion was flat compared with the previous year and well off the $58.2 billion reached in 2021.

Posthaste

Article content

Advertisement 4

Article content

BMO led the league table for full-credit bookrunner on all equity issues with 32 mandates and a deal tally of $3.3 billion, giving it a 16.72 per cent share of the business, according to Financial Post Data. The runner-up was RBC Capital Markets, the investment dealer arm of the country’s largest bank, Royal Bank of Canada, with a $2.4 billion deal tally on 28 mandates and a 12.13 per cent share.

“Overall, through the year, we managed to grind out very, very positive returns on equity markets,” said Nitin Babbar, global co-head of equity capital markets at RBC Capital Markets. “There were moments of fear based on rates moving. But the good news is that the markets, as they always do, look through the rate cycle to what the future holds…. From an activity perspective, it really was a year punctuated by windows of opportunity for new issues.”

He added that the ability to do billion-dollar transactions even in tougher times spoke to the health of the overall market.

Many of the big deals took place in energy and mining, partly driven by commodity prices, with equity issuance supporting merger and acquisition activity in the energy sector, investment bankers say.

Advertisement 5

Article content

Gibson Energy Inc., Enbridge Inc. and Pembina Pipeline Corp. were among the firms that announced billion-dollar M&A deals and large equity financings.

“In an environment where rates were rising, the M&A-driven opportunities for both Enbridge and Pembina really drove them … to market,” said Babbar, adding that the past year also showed investors believe there is a future that includes both fossil fuel and renewables.

“In previous years, it was only about renewables and moving away from fossil fuels,” he said.

The top of the rankings for corporate debt and equity deals was similar to the all-deal category, with RBC and TD on top. But BMO Capital Markets took third spot thanks to its top performance on all equity deals.

Chris John, co-head of Canadian equity capital markets at TD Securities, said uncertainty about the macroeconomic environment — how long it would take to tame inflation and where interest rates would go — tempered corporate growth plans.

“With all that was playing out through 2022 and most of 2023, companies had to be pretty conservative in how they thought about growth because you didn’t know what your access to capital was, you didn’t know what your cost of capital was,” he said.

Advertisement 6

Article content

BMO’s Miller said he expects both equity issuance and mergers and acquisitions activity to pick up later this year as the cost of capital and “hurdle” rates to generate returns come down with lower interest rates.

“That’s a big game changer for our issuing clients. And we expect that in 2024, we’re going to see issuers focus more on growth through capital projects. And through acquisitions,” Miller said.

Moreover, he added, the gap between valuations of public and private assets has also begun to close, which should help drive deal activity. Changes to private valuations traditionally lag public ones and a recovery in public markets should narrow that gap, he said, adding that he expects a pick-up in activity across sectors.

“Lower cost of capital or at least peak cost of capital should be impetus for many sectors to turn back into growth mode and be able to access the equity market,” said Miller, suggesting an early indicator can be seen in Boardwalk Real Estate Investment Trust’s successful tapping of the market in December through a bought deal of 2.2 million units at $68.50 apiece.

Advertisement 7

Article content

“I mean, the REITs have been one of the most down-and-out sectors in the equity markets because they’re long-dated assets and they’re financed heavily with leverage…. Boardwalk came and it was strongly supported by both institutions and retail,” he said.

Ben Mandell, head of Canadian M&A at RBC Capital Markets, said he anticipates more dealmaking activity in the coming year that involves pension funds and private equity players, which were relatively quiet in 2023 as they dealt with higher capital costs and uncertainty about where interest rates were going.

“I think that there’s greater stability in both of those, so I think for private equity firms, they’re seeing a more accommodating environment,” he said. “What you’ll see is a recycling of capital, so you’ll see private equity companies selling assets and then that gives them more of an avenue to go and make new investments.”

Optimism for the coming year is evident in boardrooms across North America, said Sarfraz Visram, head of the Canadian and international mergers and acquisitions at BMO Capital Markets. Despite this widespread enthusiasm, he sees plenty of worrying factors that could slow the pace of dealmaking even if 2024 is a rebound year.

Advertisement 8

Article content

Among them are potential political upheaval and ongoing geopolitical concerns that could disrupt government policy and supply chains, he said, noting the attacks by Houthi rebels on shipping vessels in Red Sea as a potential wildcard.

“We’ve got half the world’s population, or 60 countries, seeing elections this year. That’s a record,” Visram said.

On top of those political concerns, global regulators are increasing scrutiny of M&A deals, from cracking down on foreign investment to looking more closely at competition reviews. Visram said this, alongside long-term investors becoming increasingly vocal about objections to transactions, signals an end of days where announced deals are done deals.

“When you look at all those factors, combined, I think maybe we’re underestimating how dampening that might be on M&A activity for ’24,” he said.

The idea that IPOs are dead, I don’t buy that for one minute

Peter Miller, head of global equity capital markets at BMO Capital Markets

In the United States, new guidelines put in place at the Federal Trade Commission (FTC) and antitrust division of the Department of Justice will “dramatically change how the agencies consider the impact of mergers and acquisitions on competition by presuming that more transactions are anti-competitive,” according to lawyers at Torys LLP.

Advertisement 9

Article content

In a note published Jan. 3, they said the agencies will use lower benchmarks to assess whether a business combination may substantially lessen competition. Moreover, authorities will now be compelled to evaluate the cumulative effects in light of a buyer’s previous acquisitions and take into account consequences the merger may have on the parties’ employees and suppliers.

In addition to the new guidelines already in place, the lawyers noted that the FTC has called on the U.S. Congress to extend the timeline to determine whether a transaction warrants close investigation, calling the 30-day period under the Hart-Scott-Rodino Act outdated and inadequate.

Another factor that could figure into Canadian dealmaking in 2024 is the run-up to the U.S. presidential election in November, given the prevalence of inbound and outbound cross-border deals between the two countries.

“In an election year, you see M&A activity become more muted, so I do think that could have an influence in the second half of the year as relates to cross-border activity with the U.S.,” said RBC’s Mandell.

Advertisement 10

Article content

On the back of improving equity capital markets trends in Canada, prospects for a renewed IPO market will also depend to some extent on activity in the U.S., said TD Securities’ John.

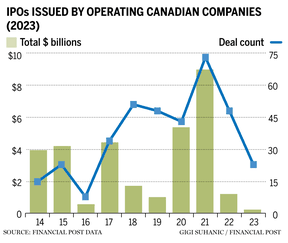

Last year there were only 23 operating company IPOs in Canada, fewer than half of the 48 registered in 2022. The total dollar value was even more undersized at just $194.6 million, a figure that is dwarfed by every other year in the past decade, including the previous low of $535.8 million in 2016, when there were only eight deals.

But there have been recent reports activity is picking up south of the border, with companies such as social media platform Reddit and fashion retailer Shein reportedly considering initial public offerings.

“If we see an increase in the U.S. market in the first couple of quarters, I think that could lead to more IPOs, maybe by the back half of 2024,” John said.

Recommended from Editorial

BMO’s Miller agrees the IPO is likely to return once market activity picks up for companies and investors.

“There are certainly some excellent companies out there who we are in dialogue with and monitoring and would make great public companies,” he said.

“The idea that IPOs are dead, I don’t buy that for one minute.”

• Email: bshecter@postmedia.com

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content