Mining at centre of more than half the equity and equity-linked deals this year

Article content

Higher commodity prices and the rise of electric vehicles made the mining sector the star of the show for Bay Street’s dealmakers in the first half of the year, with investors particularly hungry for stock and debt in companies supplying copper.

Ryan Latinovich, global head of metals and mining at RBC Capital Markets, said interest in the sector has come from both seasoned investors and those who haven’t been exposed to mining before.

Advertisement 2

Article content

“(There is) very broad support (from) new investors who may not have as long of a history in mining, but get some of the green metals thematics that are a secular driver, and want to find a way to participate,” he said. “We’ve been very fortunate to be in a leadership role with many, if not all, the biggest deals on the copper side.”

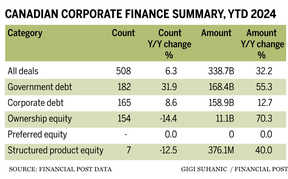

The interest in mining — the sector has been at the centre of more than half the equity and equity-linked deals this year — and a reinvigorated appetite for corporate debt helped produce 508 debt and equity deals worth $338.7 billion in the first half of 2024, according to figures compiled by FP Data, with deal count up 6.3 per cent and deal value up 32 per cent from the same period a year earlier.

On the debt side of the market, where the largest prospectus deals involved financial services companies with a smattering of telecom and energy players, buyers and sellers finally found common ground on interest rate expectations.

“People realized, I think, that rates were probably going to stay higher for longer, and so there was a lot of demand from the buyer market for product,” said Andrew Parker, co-head of the national capital markets practice at law firm McCarthy Tétrault LLP. “And issuers, even though they saw rates potentially coming down, I understand from the investment banking community that buyers were pricing in rate cuts in the bond market, so they were willing to buy, and you had sellers willing to sell, and it was just sort of off to the races.”

Posthaste

Article content

Advertisement 3

Article content

Ownership equity deal volume, though a relatively small piece of the overall dealmaking pie compared to government and corporate debt, also picked up, soaring 70 per cent to $11.1 billion even though deal count, at 154, was 14.4 per cent lower than in the first half of 2023.

“Year-to-date, mining has been the soup du jour,” said Peter Miller, head of global equity capital markets at BMO Capital Markets.

Though it is always a “busy sector,” Miller noted it was “unusual” for it to account for half the year’s issuance so far.

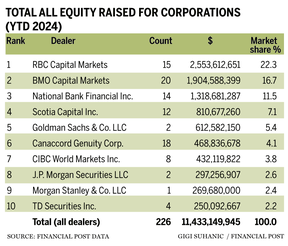

Bank of Montreal’s capital markets division had the most full-credit bookrunner mandates in the first half of the year when it came to equity deals, with 20, though its deal value of $1.9 billion and 16.7 market share trailed RBC Capital Markets. RBC had 15 deal mandates valued at $2.55 billion, putting its market share at 22.3 per cent, while National Bank Financial Inc. rounded out the top three with 14 deal mandates worth $1.3 billion and an 11.5 per cent share of the market.

Miller said most of the big-money deals in mining in the first half of the year were copper plays, including those by First Quantum Minerals Ltd., Capstone Copper Corp. and Hudbay Minerals Inc.

Advertisement 4

Article content

He noted that a comprehensive refinancing by First Quantum in February — which included a US$1.2-billion equity offering as well as a US$1.6-billion private debt offering to help fund completion of an expansion project at its Kansanshi copper-gold mine in Zambia — was “atypical” and helped drive the outsized activity.

Capstone raised $431 million in an equity offering to advance near-term growth initiatives in Chile, while funds managed by Orion Resource Partners LP sold additional shares in a secondary offering. Hudbay Minerals raised around US$400 million in the equity offering to help fund near-term growth initiatives at its Copper Mountain unit.

Maybe (Tesla) overshoots and maybe it’s undershooting now, but there’s no question that EV conversion is coming

Peter Miller, head of global equity capital markets at BMO Capital Markets

While there was activity in other parts of mining sector — especially gold and silver, whose prices are both up by double-digits in percentage terms so far this year — battery-related metals led the way, Miller said.

“There’s a little steam coming out, just look at Tesla, but, you know, we’re believers. Maybe it overshoots and maybe it’s undershooting now, but there’s no question that EV conversion is coming, and these metals will have to change the world and they’ll be needed.”

Advertisement 5

Article content

With most companies well-capitalized at this point in the cycle, more merger and acquisition-related financings would be needed to sustain the activity in the back half of the year, Miller said.

There was some M&A activity in the first half, including Equinox Gold Corp.’s acquisition of a 40 per cent stake in Greenstone Gold Mine GP Inc., purchased from funds managed by Orion Mine Finance Management for US$995 million.

Also in April, Karora Resources Inc. announced plans to merge with Westgold Resources Ltd. in a deal valued at US$786 million.

Trevor Gardner, head of global investment banking coverage at RBC Capital Markets, said he thinks there is longevity in the mini mining boom evident the first half of the year.

Gardner expects global trends in artificial intelligence and data collection and storage will increase the focus on certain metals and minerals.

“It’s hard to store or transmit energy without a lot of the critical minerals that are important to many of these companies,” Gardner said.

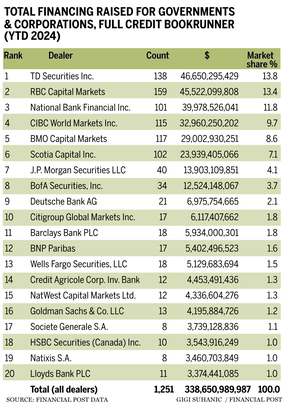

In the all-deals category, TD Securities Inc. nudged RBC out of top spot for deal value in the first half of the year, according to FP Data. While TD pulled in 138 mandates compared to 159 at RBC, TD’s deal value was slightly ahead at $46.7 billion compared to $45.5 billion at RBC, giving TD a market share of 13.8 per cent compared to 13.4 per cent for RBC. National Bank Financial rounded out the top three with 101 mandates worth nearly $40 billion and a market share of 11.8 per cent.

Advertisement 6

Article content

“The fundamentals within the mining market have been quite good and quite constructive,” said Geoff Bertram, co-head of investment banking at TD Capital Markets. “Commodities have been strong.… We’re seeing a little bit more M&A, which is helpful (and) I think we’re going to see more activity on the financing and M&A side going forward.”

He said the timing of that activity may depend on the outcomes of various election cycles playing out in Europe and the United States.

“There’s been so much election uncertainty that’s gone into the market, and the M&A is, really, an activity that you see when there’s maybe a little bit more more certainty. And we’re not quite there yet.”

Recommended from Editorial

Jeremy Fraiberg, co-chair of mergers and acquisitions at law firm Osler, Hoskin & Harcourt LLP, said there appears to be a bit of a disconnect between fundamentals and M&A activity, including a continued moribund market for initial public offerings.

“You would think that … things would come roaring back once there were rate cuts and inflation was under control,” he said. “Markets were good and so we do see activity, but I don’t know that it’s quite come all the way back to the extent that people were hoping for — yet.”

• Email: bshecter@postmedia.com

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content