")

Tim Platt/DigitalVision via Getty Images

Root, Inc. (NASDAQ:ROOT) is a property-casualty auto-insurer whose shares have seen impressive growth over the past year.

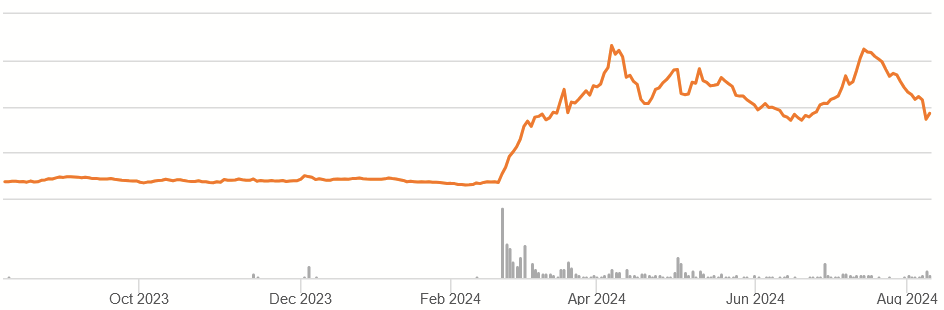

RIOT 1Y Price History (Seeking Alpha)

With Q2 results out, I thought it was worth examining if there is still some chance of undervaluation. While I think there is some merit to their business model, the current price represents most of that upside already, and it’s only a Hold until it offers a better entry price or reaches the current growth expectations.

Business Model

Dealing in property-casualty for personal auto lines, Root doesn’t exactly have a new insurance product to sell. Where they claim to have an advantage is in their data-driven approach that allows for more precise pricing. They claim to use a more unique risk model that prices based on causal factors (as opposed to correlation), one that rewards customers for good driving, while completely refusing to underwrite the riskiest drivers. As they put it in their Q2 2024 Shareholder Letter:

As mentioned, a key pillar in Root’s strategy is best-in-class pricing and automation. This means superiority in matching price to risk. We know price is the number one reason a customer chooses a car insurance company, and it is the number one reason they leave. Our modern technology and data science approach allows us to leverage machine learning and the rapid deployment of models to fine tune our prices and drive further targeted growth in our business. By monitoring our loss ratios through our automated reserving models, we can quickly update our pricing and underwriting requirements at a granular level to strike a balance between offering a competitive price and achieving target unit economics.

Another differentiating factor is their primary reliance on digital sales, largely through mobile apps or online marketplaces, relying on independent agents to a lesser extent. It was this emphasis that stood out to me most of all in their 10K.

Author’s display of 10K data

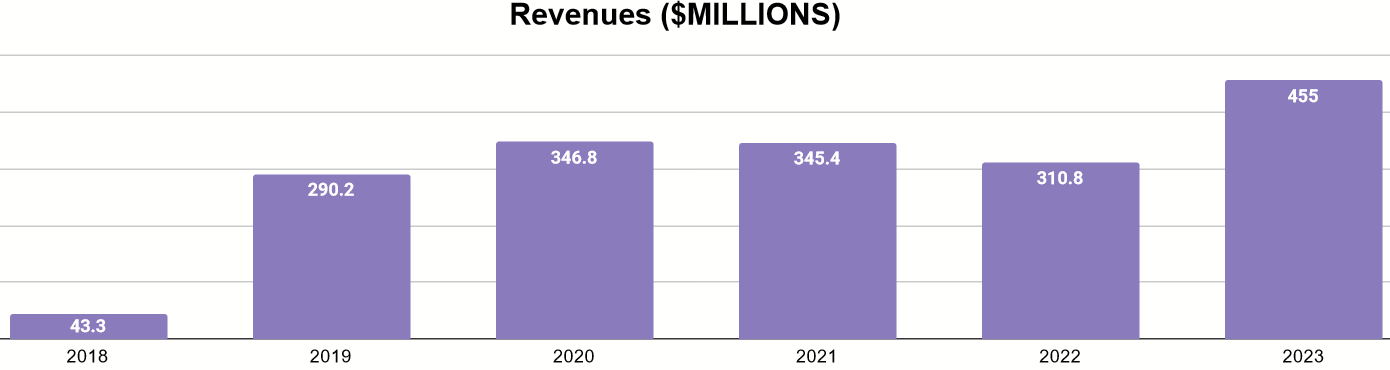

Since going public, they have been growing their business aggressively, suggesting there is some hope for them to become a contender in the auto-insurance.

Author’s display of 10K data

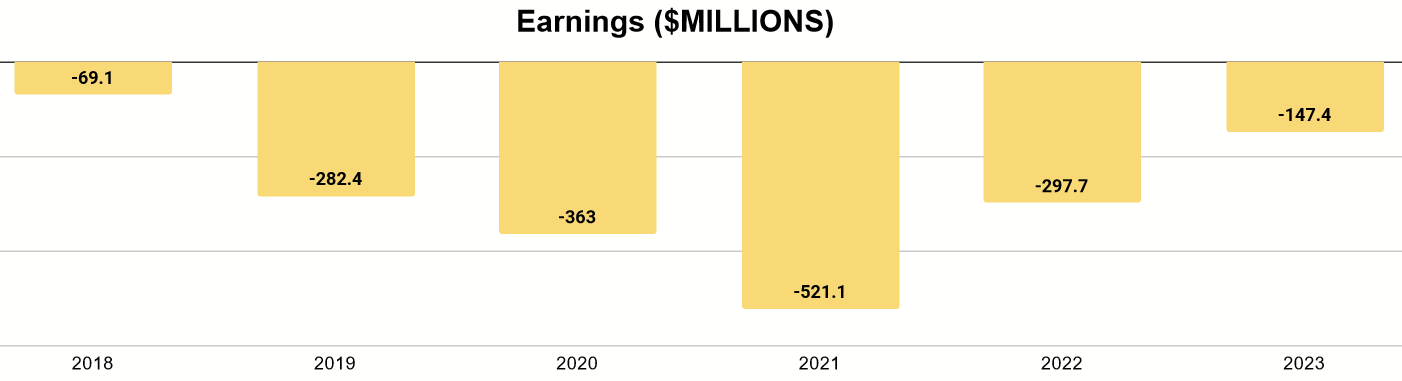

They have yet to report positive earnings, but the gap seems to be closing as their scale improves.

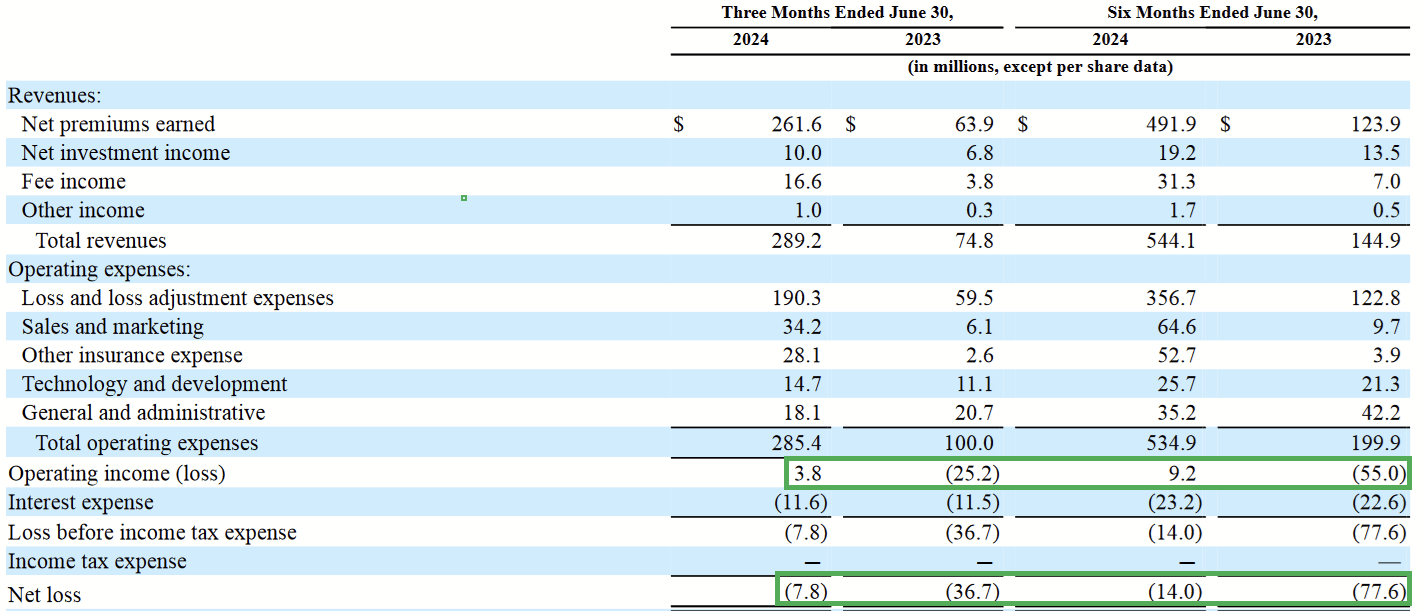

Income Statement (Q2 2024 Form 10Q)

With Q2 results, we see that they have yet to report positive net income, but a turning point appears near. Similarly, they have finally reported an operating profit. These are good signs.

Q2 2024 Shareholder Letter

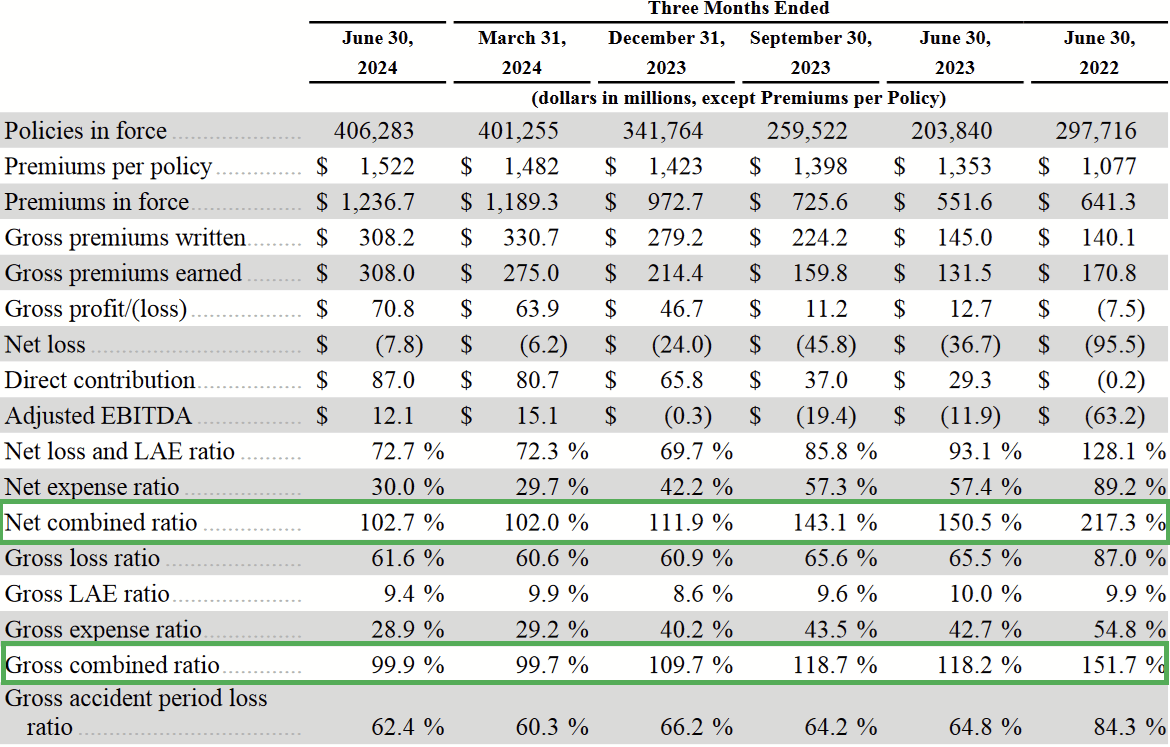

These results follow the improvement in their combined ratio over time, with recent figures putting them right on the cusp of an underwriting profit.

Future Outlook

Root currently operates in 34 states. They plan to expand into all 50, and so there is still room for growth that way, along with further saturation of their existing markets. With their digital presence and under-reliance on insurance agents, I suspect they will enjoy strong operating leverage as they grow, avoiding the huge drag on earnings that commissions can bring.

My concern is on the competitive aspect of the business. Many large insurers, such as Allstate (ALL) have been struggling recently, writing bad policies that are forcing them to cut unprofitable policies from their books. Yet, I’ve observed consolidation among the more successful big insurers, as such as Progressive (PGR). They already have a strong, digital presence and the brand recognition to support it.

Root may have an effective risk model, but it remains unclear to me why bigger insurers cannot simply adopt and implement their own models, particularly as the machine learning improved rapidly over the past year. Against businesses with stronger brands and more established distribution networks, I wonder if this might be too steep of a hill for Root to climb.

Valuation

At $46 per share, that gives ROOT a market cap of $692M for a business that hasn’t yet reported positive earnings and whose revenues are only $455M as of 2023. While it seems that profits will be reported in the next couple of years, it also seems to me that the current price likely reflects a fair value of that potential.

I think we would want to see the price decline again, perhaps to about $300M or see earnings reach close to $100M before ROOT becomes an enticing Buy. At the moment, there’s just nothing especially unique to this company to think that it deserves a huge growth premium.

Conclusion

Root seems to be following its strategy, but the current price is ahead of the curve. Investing today may produce so-so results in the long-term, but clearly the market is expecting bigger earnings before they have happened. When there are already plenty of property-casualty insurers with underwriting profits and better-known names, I am left wondering why I should be especially hungry for ROOT. For that reason, I consider it a decent Hold until the price-value works out to an actual bargain.