Top wholesale broker explains why she chose cyber, and where she sees growth

Cyber insurance has evolved remarkably since its early days – and Megan North (pictured), EVP, branch leader at Amwins, has been there for most of that journey.

“I’ve been doing cyber since before it was cool,” she told Insurance Business.

Over that period, cyber policies have transformed from basic internet liability policies to comprehensive plans that include digital crime and industry-specific enhancements.

“When I first started, the market had just a few forms,” said North. “Now, there are hundreds, updated annually, making it crucial to stay immersed in this ever-changing field.”

And it’s that change that keeps North engaged as she enjoys constant learning and the opportunity to add value through creative solutions. One significant area of growth and opportunity in cyber insurance that she sees is the SME sector.

“Any company connected to the internet has cyber risks,” she explained. “And new businesses are emerging daily, there’s really no shortage of opportunity. The most conservative estimates agree that probably a large majority of these entities do not carry cyber insurance. So the challenge in that space is going to be reaching them effectively with products that really speak to their specific needs.”

Cyber insurance disruptor

Artificial intelligence (AI) could also be a disruptor in the cyber insurance space. According to research from HiddenLayer, 1,689 AI models are currently being used by organizations, making AI security a top priority. Furthermore, 94% of IT professionals say that they’ll be dedicating funds to safeguard their AI in 2024.

“There are many conversations about AI, but we’re still figuring out its full impact on both professional and personal levels,” said North.

While the integration of AI raises numerous challenges in data protection and privacy, it also poses a threat as cybercriminals use the new tech to accelerate attacks.

“We have more questions than answers right now, but it’s clear that AI will play a significant role in the future,” added North.

North describes the current environment as a soft market – capacity is plentiful and premiums are stable or even decreasing.

“In a soft market, carriers are eager to provide more limit and capacity, sometimes offering solutions where none existed before,” she explained.

This has made the market more accessible, even for those who previously found cyber insurance too costly. But it’s not just about price.

“It’s no longer about being cheap; clients are looking for more. Carriers successful in this market are partnering with their clients, offering tools and consultations to improve security, staying proactive about the latest threats, and providing tailored solutions.”

Amwins has been trying to attract market share by launching novel products, such as Cyber Up, a cyber-triggered umbrella product designed to address exposures in industries like transportation and logistics, which traditionally face challenges in cyber-related bodily injury or property damage claims.

North also sees a growing interest from traditionally physical industries like construction, manufacturing, and agriculture. These sectors are increasingly recognizing their cyber exposures due to their reliance on technology and internet connectivity.

“Even industries that didn’t see themselves as prime targets are now exploring cyber coverage,” she told IB.

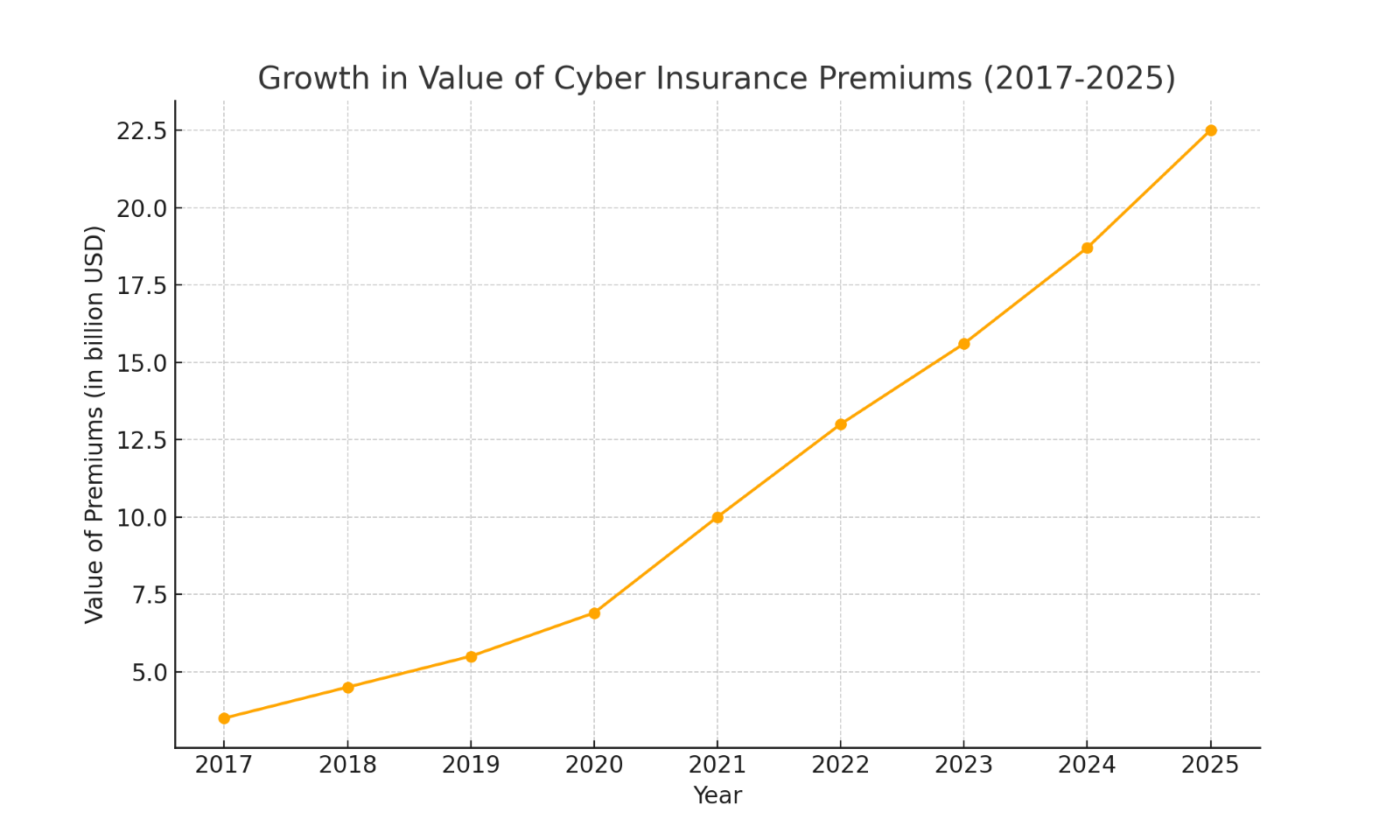

Overall, however, North is optimistic about the growth potential for the sector, telling IB that there are estimates predicting “multi-billion dollar growth in gross written premium for cyber insurance over the next few years.”

(SwissRe, 2024, 2025 forecasts)

(SwissRe, 2024, 2025 forecasts)

Despite the promising outlook, she also acknowledges the growing pains of a nascent product and the complexities that face producers.

“There’s very little standardization among cyber coverage forms, and not all carriers are comfortable providing the same level of coverage,” she said.

Unlike natural disasters, however, cyber events can be mitigated with timely interventions.

“We’re amassing more data on claims loss trends, historical risk profiles, more than ever before,” she noted. “We’re also realizing that cyber is a synthetic risk. It’s manmade. So, theoretically, there should be some ways that we can combat that. It’s not like a hurricane or weather-related event.”

So is there potential for brokerages to expand in this market? North certainly thinks so.

“The future of cyber insurance is bright, but it will require constant adaptation to new challenges and opportunities,” she said.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!