“Safety is most important,” says R. Jayakumar, 62, who works in the Chennai-based Amalgamations Group. His father started investing in SFL 25 years ago; he has followed suit. “Almost 90% of my family’s fixed deposits are in SFL. The interest rate may be slightly lower, but we get peace of mind,” he adds, as he finishes renewing his deposits here.

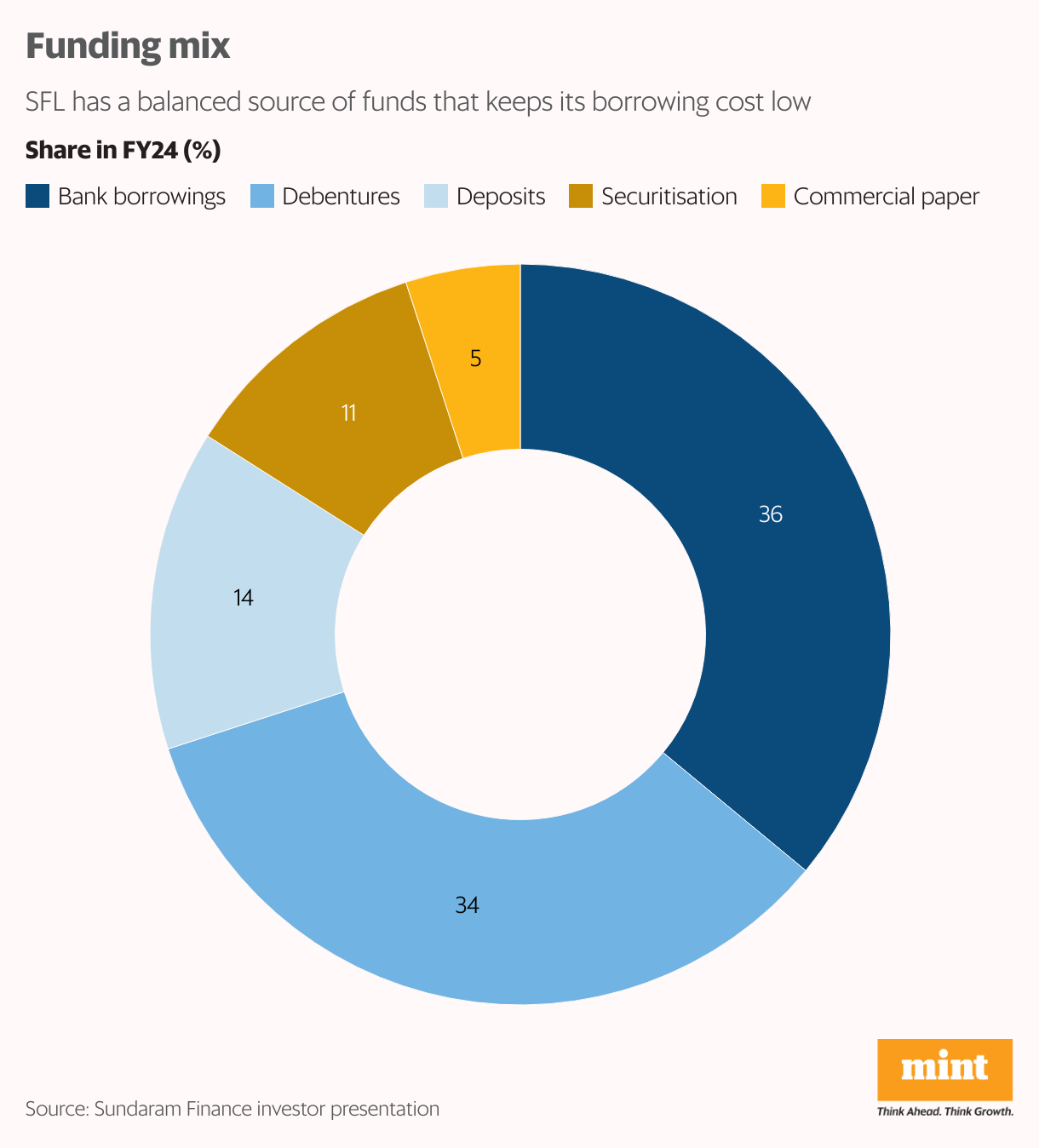

SFL, a non-banking finance company (NBFC), has 120,000 depositors. More than its AAA rating for fixed deposits, the highest safety rating, what works is the trust the company has been able to build over the years. At a time when banks are struggling to attract deposits, SFL has registered the largest-ever net accretion in deposits in 2023-24. At ₹5,800 crore, it accounted for 14% of its funding mix. The company’s executives anticipate an even higher accretion this year. This is despite SFL not actively soliciting deposits.

Some borrowers have been the company’s fans, too. “In 1977, SFL funded the purchase of my first truck, and I have not looked back since,” says Rajinder Singh, managing director, Janta Roadways. He now has 200 trucks, all car carriers. Nonetheless, he now borrows from banks as they offer cheaper interest rates—1% to 2% cheaper than SFL.“Each truck I buy costs ₹50 lakh or more, and we replace at least 20 trucks a year,” Singh reasons. But he also runs a fleet of cars that operate as taxis. They are now financed by SFL.

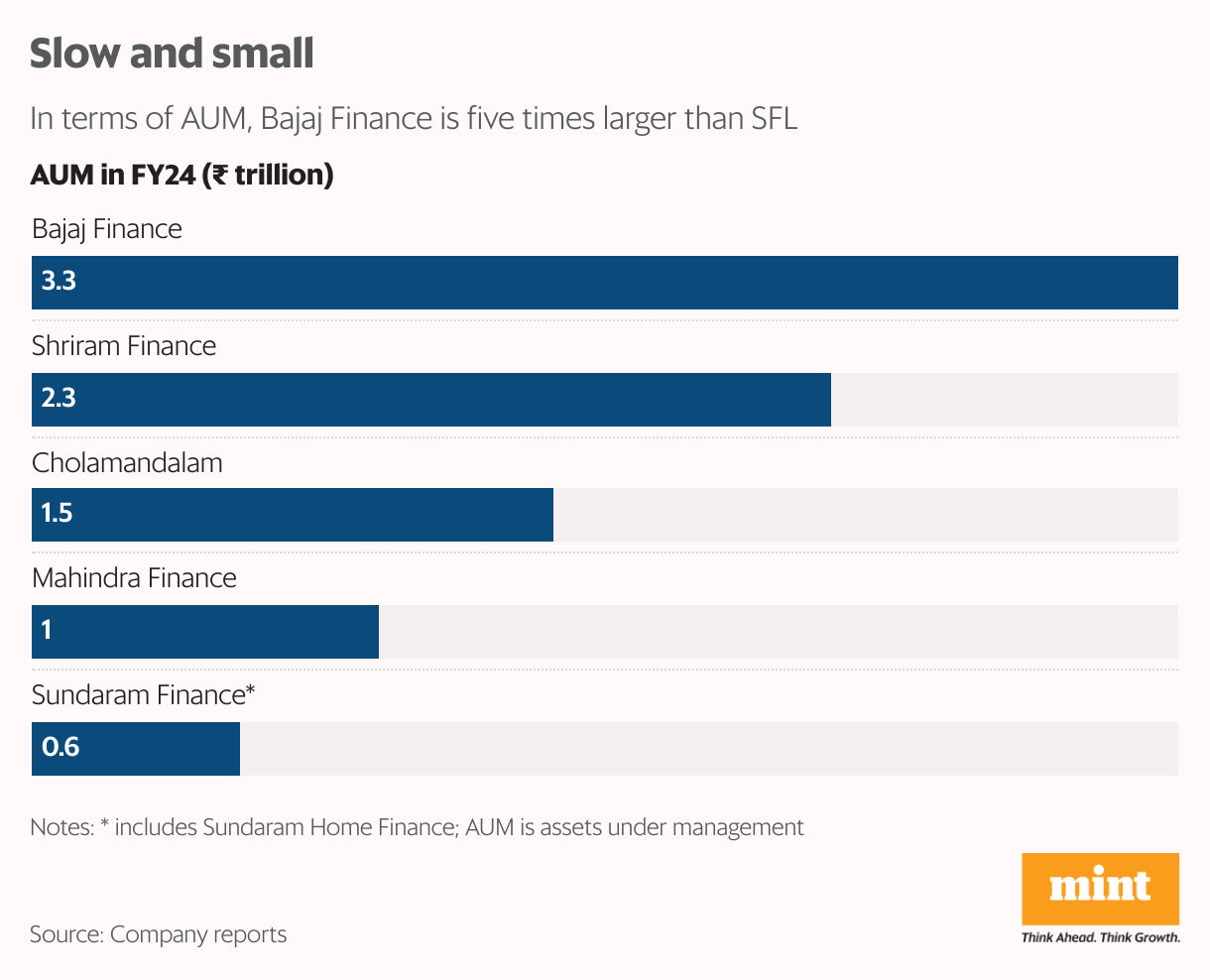

Despite the trust and goodwill that SFL has earned from its customers, it is not among the largest in the industry although it is one of the oldest. In its 70thyear of operation, its assets under management (AUM) totalled just ₹57,645 crore (including a housing business) in 2023-24. Its peers, who started off much later, have grown faster and bigger. Take the case of Bajaj Finance Ltd. In 37 years, the company has built an AUM that is five times SFL’s. Other NBFCs—Shriram Finance Ltd, Cholamandalam Investment and Finance Company Ltd and Mahindra & Mahindra Financial Services Ltd—are far bigger, too.

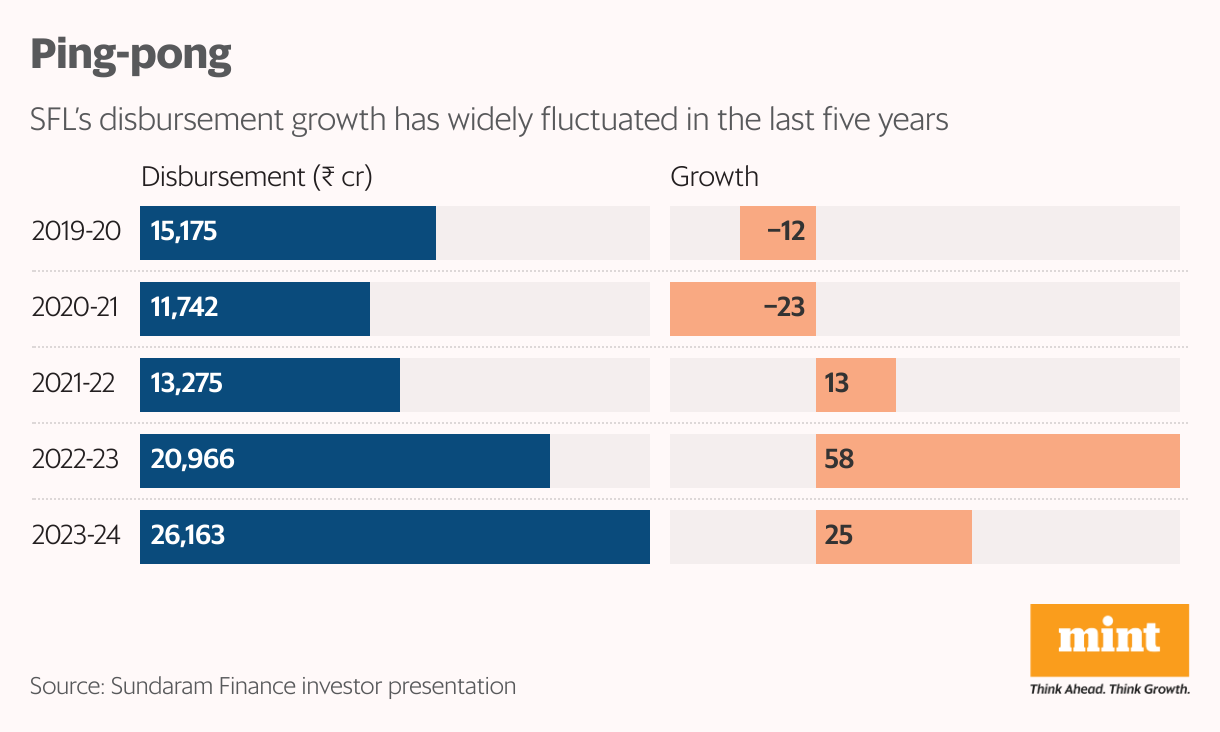

Some accuse SFL of being ‘growth phobic’ even when its disbursement last fiscal year, at ₹26,163 crore, grew by 25%. Analysts tracking the company attribute the slower built-up of AUM to its iron-clad focus on its core belief, which is to serve the underserved and conservatism such an approach has spawned. Its unique business model, which focuses on asset quality, is not primed for a fast pace of growth.

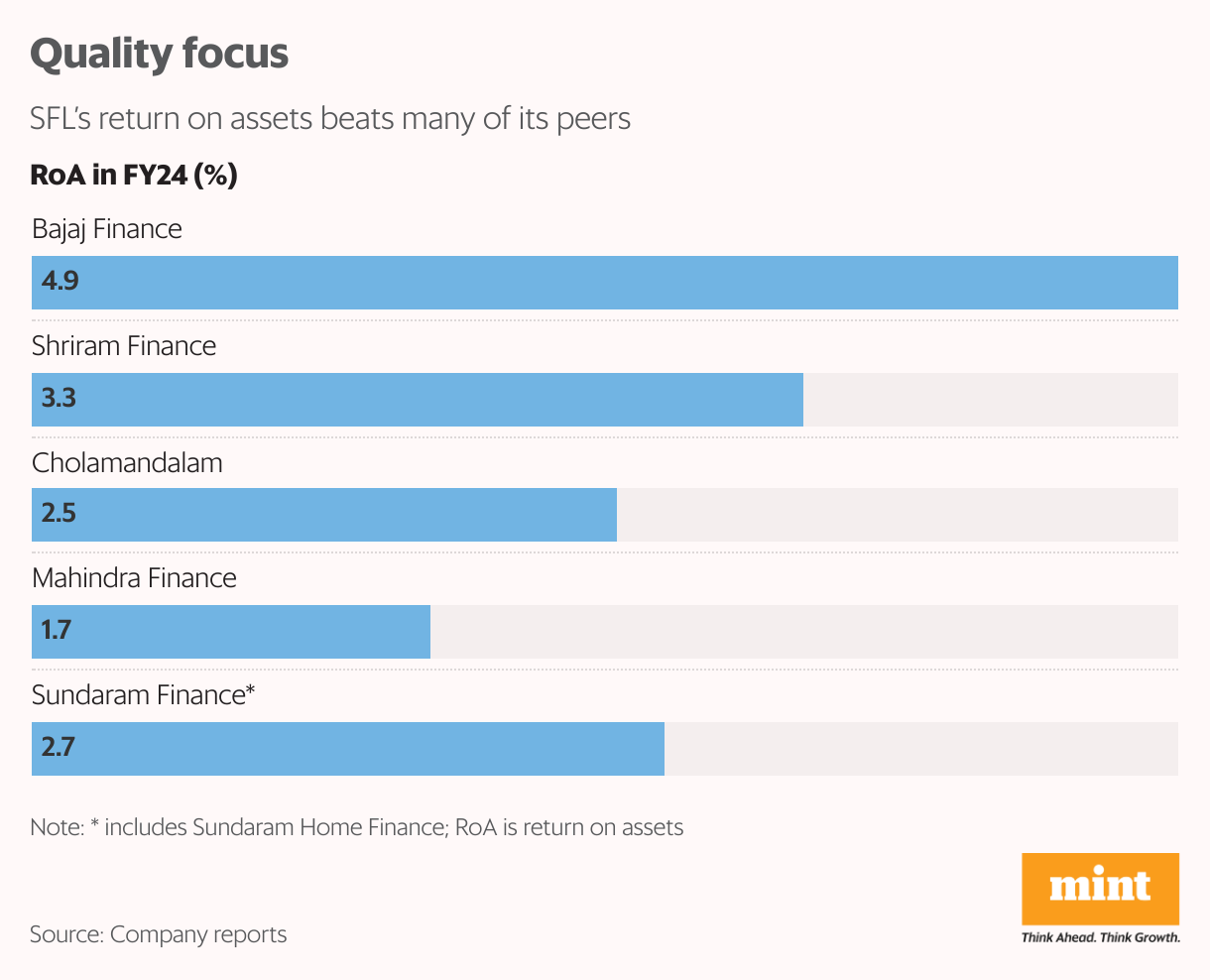

SFL’s asset quality is among the best in the industry with gross non-performing assets (NPA) of 1.3% and net NPA of 0.6% in 2023-24. Shriram Finance’s gross NPA, in comparison, is at 5.4% and net at 2.7%. SFL’s return on assets (including housing business), at 2.7%, beats Cholamandalam and Mahindra & Mahindra Financial Services.

But SFL clearly is at a crossroads. A massive transformation is sweeping the financial services sector. Regulations are being tightened for NBFCs. The Reserve Bank of India (RBI), India’s central bank, wants large NBFCs to become banks. Thus far, SFL has resisted that urge. Second, the nature of the borrowing and the profile of borrowers are changing. Indians are now borrowing, not to create assets but to fund consumption. Personal loans are growing faster than other forms of lending. SFL does not lend for consumption yet. It is, therefore, missing out on growth opportunities.

The big question: Will the market test the company’s resolve, and to what extent?

What Santhanam saw

When India gained independence, its financial sector was rudimentary. So was the transport sector, dominated by small players–those owning one or two trucks. Small truck owners were at the mercy of money lenders who charged usurious rates of interest.

T.S. Santhanam, son of TVS group founder T.V. Sundaram Iyengar, was in charge of the group’s truck and bus sales. He identified the need to fund the road transport sector and started SFL in 1954.

View Full Image

“SFL started to finance road transporters at a reasonable rate and not to maximise profits,” says Harsha Viji, executive vice chairman and great-grandson of the TVS group founder. Its lending rates are, on average, 200 basis points lower than other NBFCs even though the rates are priciercompared to banks.

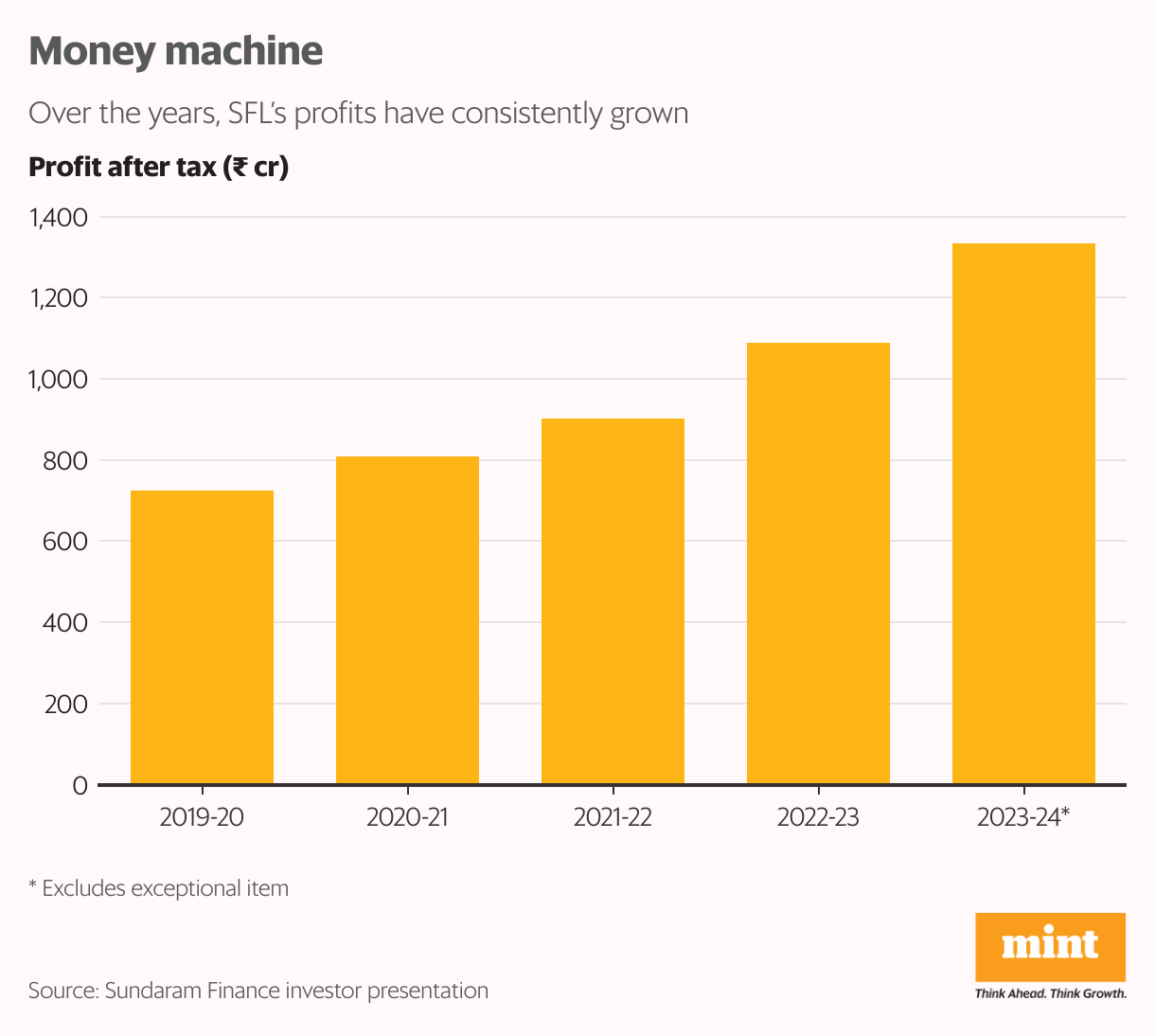

“While we may have a clear sense of mission, we are not a non-profit organization. We have made a reasonable profit from day one,” he adds.

SFL has managed this by keeping its costs low. Its average cost of funds, at 7.5%, is among the lowest in the industry as its deposits and other borrowings are AAA-rated. Its commercial papers are rated P1+. These ratings signify the highest creditworthiness and SFL is expected to easily meet repayment obligations.

“This has been possible due to prudent management, fair practices and good asset quality,” says M. Ramaswamy, the company’s chief financial officer. Its borrowing mix includes debentures, term loans, commercial papers and deposits. Credit costs, which include provisioning and write-offs, are minimal as SFL is considered to have best -in-class asset quality.

“We do not just believe in growth but growth with quality and profitability,” says Rajiv C. Lochan, managing director, SFL. Its operating cost is also among the lowest in the industry—the company eschews extravagance, he says.

Three dimensions

For the first 50 years, SFL focused only on the commercial vehicle sector. Initially, it financed small players who had just one or two trucks and then it graduated to small fleet operators. It was only in the late 1990s that the company began what it calls a three-dimensional diversification.

“We began expanding to new geographies beyond the south and outside of major transport hubs,” explains Lochan. As of March this year, SFL has 710 branches across India. South India, however, accounts for 54% of the disbursements.

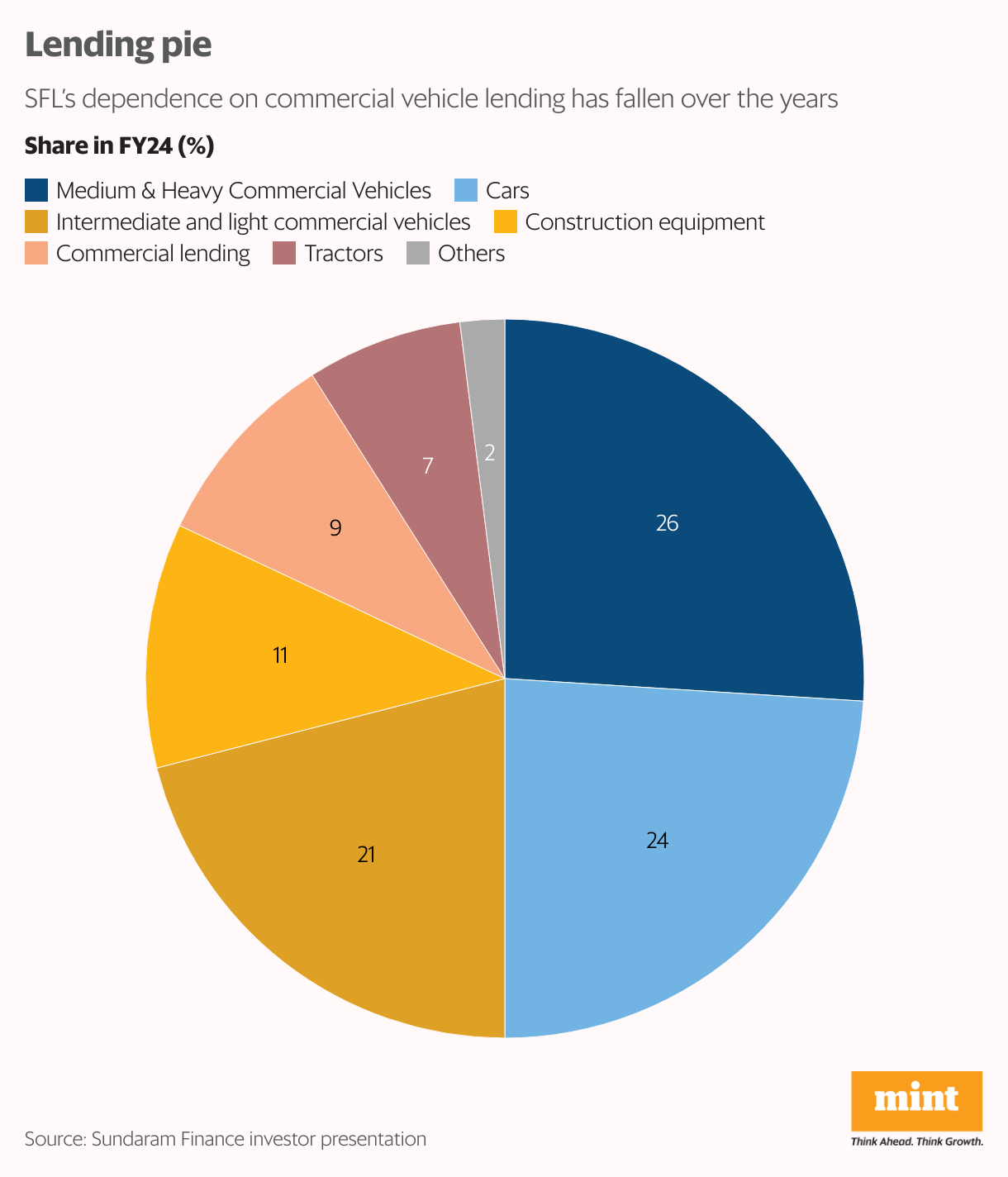

SFL then ventured beyond commercial vehicles. “We began financing the purchase of tractors, construction equipment and passenger vehicles. We also ventured into ‘without wheels lending’ in 2015-16 and began funding small entrepreneurs,” he adds. By 2023-24, commercial vehicles accounted for just 47% of the disbursement. Passenger vehicles made up 24% share; construction equipment 11%; tractors 7% and commercial lending 9% of the pie.

The third dimension in the diversification was the foray into other areas of financial services. “Royal Sundaram was the first Indian company to get a general insurance license in 2000,” adds Lochan. It was a joint venture between SFL and Royal and Sun Alliance Insurance. Apart from insurance, SFL forayed into home finance (Sundaram Home Finance) and asset management (Sundaram Asset Management Company). “We looked at life insurance very seriously but gave up as we found it too capital intensive,” says Lochan.

The clock speed

Over a 10-year period, SFL grew at a compounded annual growth rate of 10% while Cholamandalam Investment and Finance Company, which operates in the same space as SFL, jumped by 30% in the same period.

That is because SFL steadfastly continued to focus on small businesses and offered only secured loans.As we mentioned earlier, SFL eschewed consumption funding. This meant that it did not enter the personal loans space. Even in the secured asset lending space, it stayed away from gold loans and two-wheeler finance.

SFL’s business model isn’t designed for a fast pace of growth either. Branch expansion, for instance. It does not start greenfield branches in a hurry. As a rule, it first starts a sub-branch in an area seeing good demand. It is spun off into an independent branch only after a few years. This philosophy means that the NBFC’s branch expansion strategy cannot be fast-tracked. In addition, SFL is also not present in Uttar Pradesh and Bihar—states with a huge population who are underserved.

The company’s operational models also slow its growth. Unlike large finance companies, in SFL, the salesperson is also responsible for collections—both the interest and principal repayment. And every loan must necessarily have an in-person field investigation at the borrower’s residence by an SFL employee. This process is not outsourced.

“Any organization has a clock speed and if it grows faster than that, things end badly. It loses its core focus. Quality and profitability suffer,” says Lochan. “Our business model is not designed for a sprint buta marathon.”

Become a bank?

The financial services sector, which is witnessing a rapid transformation, is testing SFL’s resolve in sticking to its core belief and its conservative approach like never before. Take regulatory changes, for instance. Harmonization of regulation between a bank and NBFCs has significantly reduced the regulatory arbitrage that the latter enjoyed. Today, whether it is NPA recognition, standard assets provisioning, capital adequacy ratio and bad debts provision coverage, the regulations are either the same or tougher than banks. Like banks, NBFCs must also appoint compliance and other officers. These changes have increased an NBFC’s cost of operation.

View Full Image

Many large NBFCs now wonder if it makes sense to convert themselves into a bank—that will guarantee access to low-cost funds from current accounts that businesses open (banks pay no interest on such accounts) and savings accounts (banks pay a low interest). SFL, too, may have to take a call soon.

Market-side changes are also putting SFL in a spot. The nature of borrowing is changing and so is the profile of the borrowers. “There is a shift in consumer mindset. The young, especially, are okay with borrowing and spending to improve their lifestyle. They have the income to back it,” says Ajit Velonie, senior director, Crisil Ratings, a rating agency.

Unsecured loans by banks and NBFCs, which are predominantly personal loans, totalled ₹2 trillion in 2020-21. By 2023-24, it had more than doubled to ₹5 trillion. Despite RBI clamping down on unsecured loans by increasing the risk weightage, it grew by 35% last fiscal year. Gold loans, meanwhile, grew 20%.

How long can SFL ignore these segments?

The young are okay with borrowing and spending to improve their lifestyle. They have the income to back it.

—Ajit Velonie

Lost opportunities apart, SFL’s customer base is shrinking. As Rajinder Singh mentioned, many people are now shifting their loyalties to banks whose interest rates are 1% to 2% cheaper than SFL.“As businesses gain scale and get formalized, banks have a better handle to lend to them than NBFCs,” says Sanjay Agarwal, senior director at CareEdge Ratings, another rating agency. “New medium and heavy commercial vehicle purchase, for example, is now mostly handled by banks.”

Kipchoge’s lesson

SFL officials emphasise that they are not against change. A.N. Raju, deputy managing director, points out that apart from the diversifications in the late 1990s, SFL had started many businesses like infotech, business process outsourcing, registrar and transfer agent (sold to Kaarvy) and alternative asset business.

The company is now exploring opportunities in funding used vehicles, electric vehicles and the dairy supply chain.

What about gold loans? SFL did evaluate the business in the past but was not comfortable handling the asset because of operational complexities. Similarly, the NBFC periodically explores the bank option.“Our return on assets is better than most banks. As a bank, we will lose focus on funding the underserved,” Harsha says. The promoters, he adds, are not keen on diluting their stake—an eventuality if SFL becomes a bank considering that the maximum stake a promoter can hold in a bank is 26%. The promoter group stake in SFL is at 38% today.

Our return on assets is better than most banks. As a bank, we will lose focus on funding the underserved.

—Harsha Viji

Nonetheless, some signs of change are already visible. SFL is exploring a presence in the personal loan segment. “We believe we should be in the market at a moderate level,” says Harsha.But the company will take it slowly as personal loans have turned very risky and RBI has recently increased the risk weight for it.

The vice chairman also sees the company’s pace of growth accelerating, going ahead. He has realized the need for speed to keep up with peers. A big fan of Eliud Kipchoge, he takes lessons from the Kenyan long-distance runner’s achievements. “Kipchoge completed 42 kilometres in under two hours. This means a marathon runner need not run slowly. Time has come for SFL to increase its speed,” he says.