And it doesn’t have anything to do with the Federal Reserve

Article content

The Bank of Canada likely can’t afford to continue its current pace of interest rate cuts and will have to pick up the pace at some point as soft economic data continues to come in, according to analysts at CIBC Capital Markets.

They are forecasting the Bank of Canada will make two oversized interest rate cuts of 50 basis points — currently “pencilled in” for December and January — on the way to lowering rates to an endpoint of 2.25 per cent in June 2025.

Advertisement 2

Article content

Bank of Canada officials have already cut interest rates by 25 points three times since the beginning of June.

“There isn’t much of a reason why we think the bank needs to move this slowly. The risks to inflation are shrinking and the risks to growth are rising,” Sarah Ying, head of currency strategy at CIBC, said during a webinar on the United States Federal Reserve, Bank of Canada and the Canadian dollar.

“We think there is the possibility for an outsized move. We are less sure on when these 50s (rate cuts) will occur. That will be data-dependent.”

Jumbo-sized interest rate cuts — those larger than the standard 25 basis points — have been a hot topic in market and economic circles after the Fed cut its rate by 50 basis points last week. It was its first cut in more than four years.

Some Bay Street economists said the Fed cut paved the way for the Bank of Canada to make bigger rate reductions than it has been.

But Ying doesn’t think the Fed factors into the Bank of Canada’s rate-cut trajectory.

“It has nothing really to do with following the 50-basis-point cut in the U.S. It’s also because we need to move to normal a lot faster,” she said.

Posthaste

Article content

Advertisement 3

Article content

“Normal” refers to interest rates that create the conditions for “stable” inflation and growth.

The Bank of Canada has set a normal range for rates of 2.25 per cent to 3.25 per cent.

If policymakers were looking to get rates down to 2.25 per cent, Ying said it would take them eight more announcements to get there if they were to continue with quarter-point cuts.

“There is still a fair bit of room to go,” she said.

Ying doesn’t think the Bank of Canada has time for that, given that inflation for August came in at two per cent, which is its target, though she pointed out that the rate would be closer to 1.3 per cent if mortgage interest costs were removed.

She also said mortgage interest costs now account for a larger share of the consumer price index basket after Statistics Canada changed the weighting in May, which is “a mechanical tweak that suggests there can be some downside risk to domestic inflation if we see interest rates fall faster than the market currently expects.”

On the economic side, Canada is throwing up a lot of monthly data that is “skewed higher by population growth.”

Advertisement 4

Article content

For example, retail sales increased 0.9 per cent in July, beating analyst estimates for an increase of 0.6 per cent, and Statistics Canada offered a flash forecast of a 0.5 per cent increase in August, telegraphing a stronger third-quarter gross domestic product (GDP) than economists had previously forecast.

The latest GDP data pointed to stalling growth in June and July, but Ying said there is reason to be skeptical of the strength of those numbers.

“If you look on a per-capita basis, retail sales fell 1.3 per cent from a year ago in real terms,” she said. “It’s all about per capita. That’s really the highlight of the Canadian data.”

The Bank of Canada has also acknowledged the role population growth plays in the data. For example, in the central bank’s latest Monetary Policy Report, third-quarter GDP is forecast to come in at 2.8 per cent, assuming population growth of three per cent.

“That effectively erases all the growth we see in the (central) bank’s GDP forecast on a per-capita basis,” Ying said.

Households are also allocating more of their income to debt servicing and less to consumption, and “labour market slack is also comparatively worse than it is in the U.S.,” she said. “That’s really the story in Canada that the data per capita is slowing down. It just seems the balance of risks seems a bit more asymmetrical here.”

Advertisement 5

Article content

Sign up here to get Posthaste delivered straight to your inbox.

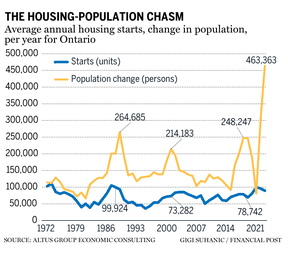

The Greater Toronto Area’s (GTA) housing crisis is intensifying, with new data revealing that high municipal fees and prolonged approval processes are driving up the cost of new homes.

The latest Municipal Benchmarking Study from the Building Industry and Land Development Association (BILD), developed by Altus Group Economic Consulting, warns that the region’s housing supply is lagging dangerously behind population growth, signaling an impending crisis if immediate action isn’t taken.

According to the study, the gap between housing stock and population growth in the GTA is the widest it has been in over 50 years. — Shantae Campbell, Financial Post

- Today’s data: U.S. new homes sales and mortgage applications

- Earnings: Jeffries Financial Group Inc., AGF Management Ltd.

Advertisement 6

Article content

Recommended from Editorial

A core principle of taxation is that taxpayers have the right to pay no more — and no less — than what is required by law. But what happens if the government proposes a new taxation law to be effective immediately (or at a later date) and the proposed law itself is in flux or, worse, hasn’t even been fully drafted? Or if flawed draft legislation has been released and requires significant changes? In such situations, how are Canadians supposed to plan their financial affairs when the rules they are expected to follow are unclear or incomplete? Read Kim Moody here.

Build your wealth

Are you a Canadian millennial (or younger) with a long-term wealth building goal? Do you need help getting there? Drop us a line at CVarga@postmedia.com with your contact info and your goal and you could be featured anonymously in a new column on what it takes to build wealth.

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Today’s Posthaste was written by Gigi Suhanic, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content