High prices continue to hit Canadians where it hurts the most

Article content

You could almost hear the collective sigh of relief when inflation hit the Bank of Canada‘s 2 per cent target — after all we’d been waiting three years.

August’s reading was the slowest increase in the consumer price index since February of 2021, opening the door for the central bank to bring more relief to Canadians struggling under higher interest rates.

However, as good as hitting the target is, it is not a magic bullet — mainly because 2 per cent inflation today is a lot different than 2 per cent in 2019, say Royal Bank of Canada economists in a recent report.

Advertisement 2

Article content

“The composition of what’s driving prices looks very different now than it did before the pandemic, and in some ways, it is less healthy for the economy,” said the team led by chief economist Frances Donald.

Today’s inflation continues to hit Canadians where it hurts the most.

Two thirds of growth in inflation in August was mortgage interest costs and higher rents compared to two per cent growth on average in the decade before the pandemic, they said. Growth in mortgage costs will slow as the Bank of Canada cuts rates, but Canadians can expect less relief when it comes to home and rent costs that will stay high because of the housing shortage and growing population.

Food prices are another pain point. Even though this price growth is slowing, grocery prices are still up 25 per cent from before the pandemic.

“For many Canadians, especially lower-income families, housing and food prices remain the most critical categories for price growth,” said the economists. “One could argue that 2019’s 2 per cent inflation was a more favourable composition than 2024’s 2 per cent.”

Posthaste

Article content

Advertisement 3

Article content

Another reason 2 per cent inflation today weighs more heavily on Canadians than it did before the pandemic is that in this case, what goes up, doesn’t come down.

“Prices are 17 per cent higher than they were the month before the pandemic, and 2 per cent inflation means they are still climbing, just at a slower pace,” said the economists.

Wage growth, up 18 per cent, has helped ease the strain, but there is the risk that if interest rates stay too high too long this growth could slow again while prices remain high, they said.

In the battle against inflation so far much of the decline has been due to the unwinding of pandemic shocks, but going forward downward pressure will likely come from “more painful places in the economy.”

Canada’s labour market is weakening, with the unemployment rate already a percentage point higher than before the pandemic. While household savings are still high they are mostly held by higher-income households who aren’t as likely to spend them.

“With households stretched by a high cost of living and softening labour markets, disinflationary forces will be symptoms of a struggling economy, instead of a ‘normalization,’” said RBC.

Advertisement 4

Article content

One “silver lining” they said, is it gives the Bank of Canada plenty of room to take interest rates lower.

Sign up here to get Posthaste delivered straight to your inbox.

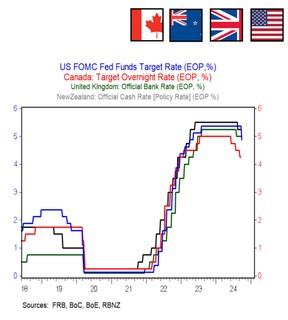

They were the most aggressive hikers on the way up, but these four major central banks are taking different paths on the way down, points out Douglas Porter, chief economist at BMO Capital Markets, who brings us today’s chart.

At 5.2 per cent, the Reserve Bank of New Zealand now has the highest interest rate of the four after the United States Federal Reserve slashed 50 points off its rate last month.

The Fed is now even lower than the Bank of England after the latter held steady at 5 per cent at its recent meeting.

U.S. short-term rates haven’t been below the U.K.’s since June 2022, and the pound got a lift as a result, said Porter.

The Bank of Canada, meanwhile, started veering off from the pack in 2023 and is now the lowest rate among the four at 4.25 per cent.

What’s more — the “supersized Fed move opens the door wide for the BoC to match, data permitting,” said Porter.

- Air Canada’s pilots begin voting today on a tentative labour agreement. The ratification vote closes Oct. 10.

- Canada’s tech community will gather today through Thursday in Toronto for the Elevate conference. Speakers include Shopify Inc. president Harley Finkelstein and Lightspeed Commerce Inc. CEO Dax Dasilva.

- Calgary is expected to report home sales for September today followed by Vancouver on Wednesday and Toronto on Thursday.

- Today’s Data: United States construction spending, ISM manufacturing

- Earnings: Nike Inc, Paychex Inc, McCormick & Co Inc

Advertisement 5

Article content

Recommended from Editorial

A couple in their mid-40s with two young children want to retire early, especially after recently learning about the medical histories in both their families. Although they are both healthy now, they want to enjoy their lives to the fullest. We asked financial planner Graeme Egan to help them out. Find out more

Build your wealth

Are you a Canadian millennial (or younger) with a long-term wealth building goal? Do you need help getting there? Drop us a line with your contact info and your goal and you could be featured anonymously in a new column on what it takes to build wealth.

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Plus check his mortgage rate page for Canada’s lowest national mortgage rates, updated daily.

Today’s Posthaste was written by Pamela Heaven, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content